Visa Inc. (V) is set to launch the largest initial public offering in U.S. history on Wednesday but I doubt it will do much to help this market (from a bullish standpoint). The company is offering 406 million shares with an anticipated price between $37 and $42, according to SEC filings.

In total, the IPO could raise nearly $17 billion, surpassing the record held by the AT&T Wireless IPO from 2000 which raised $10.6 billion. The $15 to $17 billion projection is approximately 70% higher than what the market was reporting when I was anticipating this IPO last November.

“VISA, the largest U.S. credit card network said it is looking to raise $1o billion in an initial public offering, according to a registration statement with the SEC.”

JPMorgan (JPM) is one of the lead underwriters (Goldman Sachs is the other) so the market wants this IPO to launch successfully so additional fears don’t rise following the $2 Bear Stearns fire sale. A successful IPO would generate a large cash influx to banks such as JPMorgan, Bank of America and Citigroup. Visa’s IPO could generate around $500 million in fees for underwriters, according to documents with the SEC.

Shares will price after the close Tuesday with lots ready to move Wednesday morning.

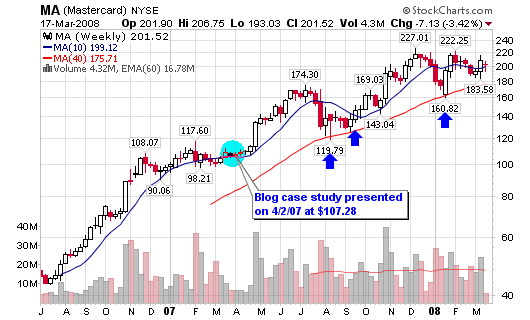

As pointed out in my last post, Visa and Mastercard (MA) are not directly exposed to rising defaults and late-paying consumers because they process transactions and these transactions typically rise when credit is tight from banks. American Express and Discover are not as fortunate in this sense as they extend the credit to their card holders, exposing themselves to the defaults.

As you can see, Mastercard (MA) has held up very well during this credit crisis. It has not violated it’s major moving averages and is still in an overall long term up-trend.

November 15, 2007: Anticipating the VISA IPO

Why do I like VISA’s potential?

- $1o Billion would represent the second largest IPO ever!

- Revenues are expected to grow steadily as consumers continue to use their cards

- VISA processed 44 billion transactions totaling $3.2 trillion in 2006 (Mastercard processed 23.4 billion transactions totaling $1.9 trillion)

- VISA has made $771 million on $3.7 billion in revenue during the first nine months of 2007

- VISA makes their money from the fees it charges to card users and merchants using its network

- Mastercard is half the size of VISA and is up 5-fold from its IPO

BEST OF ALL:

- Because it acts as an intermediary, Visa doesn’t sustain losses when consumers don’t repay the debts run up on credit cards bearing its brand. Those liabilities instead fall to the banks that issue the cards and set the terms of repayment

- Most of Visa’s major stockholders are banks. They include: J.P. Morgan Chase & Co., which owns 23.3 percent of the company’s Class B Stock; Bank of America Corp., 11.5 percent; National City Corp., 8 percent; Citigroup Inc., 5.5 percent; U.S. Bancorp, 5.1 percent; and Wells Fargo & Co., 5.1 percent.

NO RISK for VISA; the banks are responsible for the cardholders that don’t pay their bills. What could be better than that? Tell me!

Connect with Me