Stock of the Day

Maidenform Brands

Friday’s Intra-day Price: MFB – $20.77

Next Earnings Date: Wednesday May 9, 2007

Sector: Consumer Discretionary

Industry: Apparel, Accessories & Luxury Goods

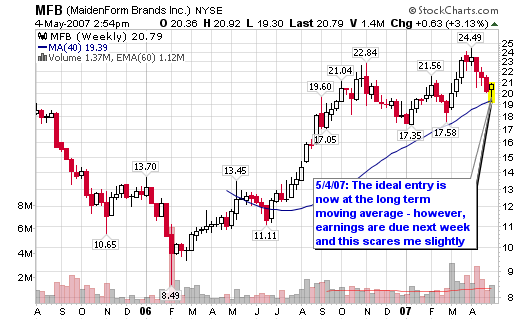

52-wk Range: $24.49 – $11.11

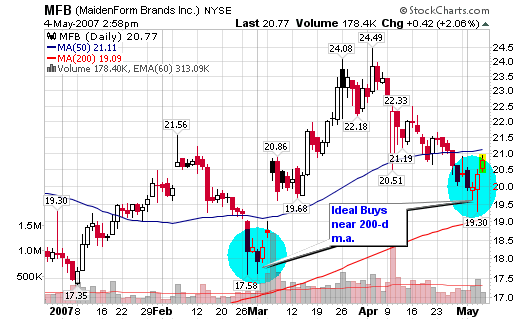

So what do we have? The technical aspects of this company look excellent with the ideal entry right now at the 200-d moving average. The stock has held the line as support two times over the past several months and looks to be a solid long term young stock. The strongest growth stocks are usually within 3-5 years of their IPO and MFB fits this criterion by debuting less than two years ago.

However, earnings are due to be announced next week and based upon Under Armour’s (AU) recent disappointment, I would be cautious. As of this writing, I have not added shares and do not own the stock personally. I will setup my risk-to-reward ratios this weekend and make the decision heading into Monday morning’s opening. I want to own the stock and now is the ideal point to accumulate shares but earnings scare me.

I don’t need to get caught in a severe gap-down that completely screws my risk factor and blows past my stop. If UA reported better expectations, I would be all over these shares right now. Other than that, the stock looks good heading into the future.

Institutional Analysis:

Held by Institutions: 70.59%

Money Market: 107

Mutual Fund: 161

Other: 8

New Positions: 62

Positions Sold: 21

Shares Held Current Period: 26.7mm

Shares Held Previous Period: 21.2mm

Shares Bought: 10.0mm

Shares Sold: 4.5mm

Value of Shares bought: $206.2mm

Value of Shares Held: $93.7mm

Top Five Institutional Holders; Shares Held

Credit Suisse; 2,643,318

Barclays Global Investors UK Holdings Ltd; 1,553,596

Putnam Investment Management, LLC; 1,184,480

Morgan Stanley; 1,150,956

Wells Fargo & Company; 1,099,114

Key Fundamental Numbers:

Market Cap.: $477.8mm

Outstanding Shares: 22.98mm

Short Ratio: 2.21

Operating Margin: 6.66

EPS: 1.15

ROA (%): 10.73

ROE (%): 41.88

P/E (TTM): 17.38

P/E (Forward): 14.84

Price to Sales Ratio: 1.10

Book Value per Share: 3.28

PEG Ratio: 0.99

Price to Book Ratio: 6.10

Debt/Equity: 1.47

Cash Flow/Share: 1.43

Next Quarter 0.27

Next Year 1.11

Earnings:

Yearly (2006): 1.15

Yearly (2005): (0.39)

Yearly (2004): 0.30

Revenue (millions):

Yearly (2006): 416.8

Yearly (2005): 382.2

Yearly (2004): 337.0

Company Profile:

Maidenform Brands, Inc. and its subsidiaries design, source, and market a range of intimate apparel products in the United States and Canada. Its products include bras, panties, and shapewear. The company offers its products under the Maidenform, Flexees, Lilyette, Sweet Nothings, Rendezvous, Subtract, Bodymates, and Self Expressions brand names. Maidenform Brands sells its products through department stores; national chain stores; mass merchants, including warehouse clubs; and specialty retailers, licensing income, and off-price retailers, as well as through company-operated outlet stores and Web sites. As of December 31, 2006, it operated 76 outlet stores. The company is headquartered in Bayonne, New Jersey.

Related Stock: UA, Under Armour (currently getting hit hard near the 200-d moving average).

Bottom Line: The stock is a buy right now between $19 and $21 but earnings will be a “hold-your-breath” time come next week. I’ll let you know if I jump in on Monday!

Chris, the earnings and revenue deceleration does not bother you? Especially, the revenue decleration considering the high debt level?

Pleadership,

A few things are suspect and that is why I did not buy today and will research further this weekend (especially with earnings due). Aside from fundamentals, the ideal technical accumulation (buy) is right now!

Yes, I agree that technically I see this as being very attractive. Although, a few points:

* Industry group (IBD groups) has been losing interest. 3 months ago it was 17/197, last week 70/197 and the group surrently sits at 105/197. MFB is not even in the Top 5 of overall rating in the group.

* You you pointed out about AU, but COH also disapointed the street and this is probably the best stock in the group.

* MFB posts a C- in ACC/DIS and not only has revenues slowed but last quarter they posted the lowest EPS compared to the last 6 quarters (except March ’06).

A couple of stocks I have had on my radar as of late have been VCP, RKT, KAI, TIN, and SEO (Paper Group) which have been gaining favor overall and BRLC. BRLC was mentioned in IBD New America and, Eventhough it is an eratic chart, has posted positive EPS the last two qtrs on increasing revenue. Have you taken a look at any of these and if so, what are your thoughts?

Have a great weekend!

Since there was not a post about this is it safe to assume you did not purchase this?

Albert,

I have not established a position and will not after further analysis. I will wait to see what happens after the release.

Any thoughts on the rest of my comments regarding the specific stocks?